Standing in a room full of water while watching your prized possessions soak in a sudden flood is an emotional experience that leaves most Glendale homeowners feeling completely helpless. Once the initial shock wears off, the focus inevitably shifts toward the financial recovery and the complex maze of insurance paperwork that follows. Navigating water damage restoration glendale ca insurance claims requires a strategic approach, as the language in your policy often dictates the difference between a fully funded restoration and a massive out-of-pocket expense. In 2026, California insurance regulations have become more nuanced, requiring precise documentation and a deep understanding of what constitutes a “sudden and accidental” event. This guide serves as your definitive resource for understanding the relationship between your homeowners policy and the professional services needed to return your property to its pre-loss condition in the Jewel City.

Does homeowners insurance cover water damage in California?

In most cases, homeowners insurance in California does cover water damage, provided that the cause of the loss is considered sudden and accidental rather than the result of long-term neglect. When you begin the process of water damage restoration glendale ca, your insurance adjuster will primarily look for the source of the leak to determine eligibility. Standard policies typically cover events such as a burst pipe, a washing machine hose failure, or a water heater rupture that happens without warning. However, they often exclude damage caused by “seepage” or “gradual leaks” that have been occurring over a period of weeks or months, as these are classified as maintenance issues.

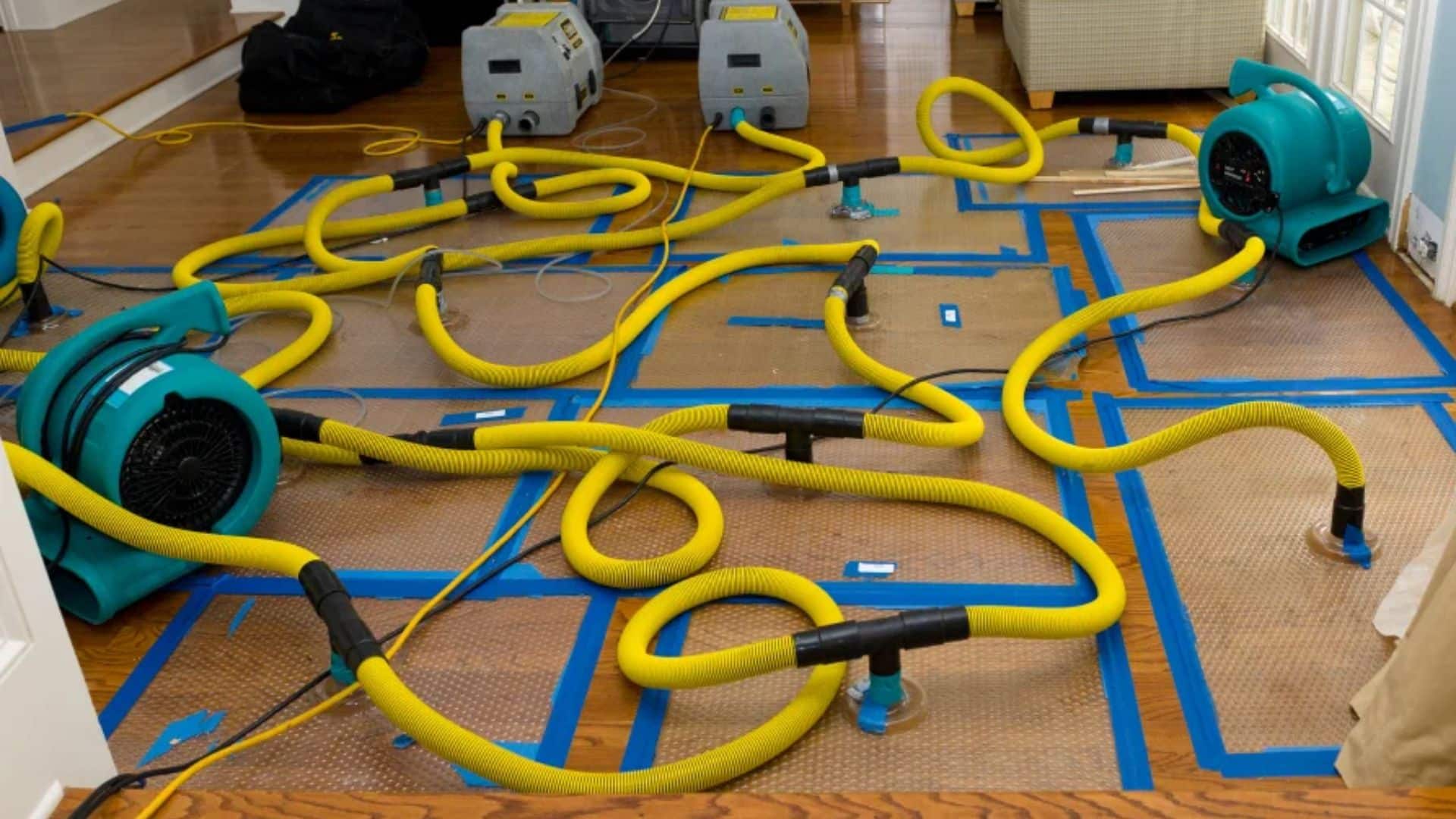

The key to a successful water damage restoration glendale, claim is immediate action and professional verification. Insurance companies expect policyholders to mitigate the damage as soon as it is discovered to prevent further loss, such as the growth of mold or the warping of structural subfloors. By hiring a certified restoration team immediately, you demonstrate that you are taking the necessary steps to protect the property, which often makes the claims process smoother. Professional documentation, including moisture maps and thermal imaging, provides the objective evidence that adjusters need to justify the costs of industrial drying equipment and labor.

Navigating Glendale Water Damage Insurance Claims Successfully

Filing Glendale water damage insurance claims involves several critical steps that must be performed in a specific order to ensure maximum coverage. First, you must notify your insurance carrier to open a claim and receive a claim number, which will be the primary identifier for all future correspondence. Next, you should avoid throwing away any damaged items until an adjuster has had a chance to inspect them or until they have been thoroughly documented by your restoration contractor. This visual proof is essential for the “Personal Property” or “Contents” portion of your claim, ensuring you are reimbursed for ruined furniture, electronics, and clothing.

Understanding Sudden vs. Gradual Leaks

Insurance policies are designed to protect against unforeseen disasters, not the natural aging of a home’s plumbing. If a pipe bursts under your sink while you are at work, it is a sudden event that is almost always covered. Conversely, if a window has been leaking slightly every time it rains for three years and has caused the wall to rot, the insurance company may deny the claim based on a lack of maintenance. Distinguishing between these two scenarios is often the most contentious part of a water damage claim in Southern California.

The Role of the Deductible in Your Claim

Your deductible is the portion of the restoration cost that you are responsible for paying before the insurance company begins to contribute. In the Glendale area, deductibles are often set at $1,000 or $2,500, though some “high-risk” policies may have higher amounts. It is important to remember that the deductible is paid directly to the restoration contractor, not to the insurance company. Understanding your deductible early in the process helps you budget for the immediate out-of-pocket expenses while the larger claim is being processed.

Understanding Coverage for Flooding Glendale Residents Need

When discussing coverage for flooding Glendale, it is vital to understand that standard homeowners insurance specifically excludes damage caused by “rising groundwater.” This is a major point of confusion for residents living near the Verdugo Mountains or in low-lying areas during heavy rainstorms. If water touches the ground outside your home before entering through a door or window, it is legally defined as a flood. To have protection against this type of disaster, you must have a separate flood insurance policy, typically provided through the National Flood Insurance Program (NFIP) or a private flood carrier.

In 2026, many Glendale residents are also adding “Water Backup” endorsements to their standard policies. This specific coverage protects you if a city sewer line backs up into your home or if a sump pump fails. These events are not covered by standard homeowners insurance or standard flood insurance, making the endorsement a critical safety net for homes with finished basements or those in older neighborhoods with mature tree roots. Discussing these specific coverage gaps with your agent before a disaster occurs is the best way to ensure your property is fully protected.

Identifying Perils and Exclusions

Every insurance policy has a list of “covered perils” and “exclusions” that define what is and isn’t a valid claim. Common covered perils include fire, lightning, and windstorms. However, many policies exclude “earth movement,” which can be a concern for hillside properties in Glendale. If a water pipe breaks because of a minor earthquake or soil shifting, you may need an earthquake endorsement to cover the resulting water damage. Reading the “Exclusions” section of your policy is the most important step in understanding your true level of risk.

The Difference Between Replacement Cost and Actual Cash Value

When you receive your payout, it will be calculated based on either “Replacement Cost Value” (RCV) or “Actual Cash Value” (ACV). RCV pays for the cost to replace your damaged items with brand-new equivalents at today’s prices. ACV, on the other hand, subtracts depreciation based on the age of the item. In Glendale’s luxury real estate market, having an RCV policy is highly recommended, as it ensures you can actually afford to rebuild your home to its original standard without a significant financial shortfall.

Coordinating with Public Adjusters

If your insurance claim is particularly large or complex, you may consider hiring a “Public Adjuster.” Unlike the insurance company’s adjuster, a public adjuster works for you and takes a percentage of the final settlement. While they can be helpful in negotiating higher payouts for complicated structural losses, many Glendale homeowners find that a reputable restoration contractor can provide the same level of documentation and advocacy without the extra fee. You can explore our professional assessment services by visiting our contact page to see how we help document your loss for the carrier.

A Step-by-Step Guide to Filing Restoration Claims CA Residents Can Follow

The process of filing restoration claims CA residents face is governed by the California Fair Claims Settlement Practices Regulations. These laws require insurance companies to acknowledge your claim within 15 days and provide a decision on coverage within 40 days of receiving all necessary documentation. To speed up this process, you should maintain a “claim diary” that records the date and time of every conversation you have with your insurance company, along with the name and title of the person you spoke with. This log is invaluable if there are any disputes later in the process regarding what was promised or authorized.

Your restoration contractor will play a pivotal role in this process by providing the “estimate” that the insurance company will review. Most professional firms in Glendale use a software called Xactimate, which is the same tool used by the insurance adjusters themselves. This ensures that the pricing for every “line item,” from the cost of a square foot of drywall to the hourly rate for a technician, is consistent with local market rates. By using the same language and pricing structure as the insurance company, the contractor minimizes the friction between the estimate and the final approval.

Documenting the Scene Before Repairs

Never allow a contractor to begin demolition before you have captured comprehensive photos and videos of the standing water. You want to show the depth of the water and the exact points where it entered the structure. If possible, keep the “failed part,” such as the burst pipe or the cracked supply line, as the insurance company may want to inspect it to determine if there is a subrogation opportunity against the manufacturer of the faulty part.

Authorizing the Work and the “Direction to Pay”

When you hire a restoration company, you will sign a “Work Authorization” form. This gives the company permission to enter your home and perform the necessary drying services. Many homeowners also sign a “Direction to Pay,” which allows the insurance company to send the checks directly to the restoration contractor. This is a common practice in Glendale as it simplifies the financial transaction and ensures the crew is paid promptly, but you should always review the final invoice before the last check is issued.

Managing the Rebuild Phase

Once the home is dry, the “mitigation” claim is usually closed, and a “rebuild” claim is opened. This covers the cost of hanging new drywall, painting, and installing new flooring. It is important to ensure that the rebuild estimate matches the quality of the materials that were removed. If you had custom solid-oak floors, the insurance company is obligated to pay for solid-oak floors, not a cheaper laminate alternative. Your contractor will help you advocate for “like-kind and quality” replacements during this final stage of the recovery.

| Insurance Term | What It Means for You | Why It Matters |

| Sudden & Accidental | The damage happened without warning | Requirement for coverage in standard policies |

| Mitigation | Steps taken to prevent further damage | Required by policyholders to avoid claim denial |

| Additional Living Expenses | Coverage for hotels and meals | Essential if your home is uninhabitable during drying |

| Water Backup | Coverage for sewer and drain failures | Often requires a separate rider or endorsement |

Why Professional Documentation is the Key to Full Coverage

The success of any water damage restoration glendale ca insurance claim rests on the quality of the data provided to the adjuster. In 2026, “subjective” assessments are no longer enough; insurance companies require “objective” data. This means providing printouts of daily moisture readings from every affected room and thermal images that prove moisture is gone from inside the wall cavities. Professional restoration firms invest thousands of dollars in these tools specifically to ensure that their clients’ claims are approved without delay or “haircuts” to the estimate.

Furthermore, professional documentation protects you from future liability. If you ever decide to sell your Glendale home, you are legally required to disclose any previous water damage. Having a “Certificate of Completion” and a full “Drying Log” from a certified firm proves that the damage was handled correctly and that the house is safe and mold-free. This documentation maintains your property value and provides peace of mind to future buyers, making the professional route a much smarter long-term investment than “DIY” drying.

The Importance of Air Quality Testing

In many insurance claims, the cost of post-remediation air quality testing is covered. This involves an independent third party taking air samples to ensure that the mold spore count inside your home is lower than or equal to the outdoor air. This is the ultimate proof that the restoration was successful. While it adds a small cost to the claim, most insurance adjusters in the Glendale area approve it as part of a comprehensive “clearance” protocol, especially in homes with young children or elderly residents.

Dealing with “Preferred Vendor” Programs

Your insurance company may suggest a list of “preferred vendors” for your restoration. It is important to know that under California law, you have the right to choose any contractor you want. While preferred vendors have a pre-existing relationship with the insurance company, independent contractors often provide a more personalized level of service and act as a stronger advocate for the homeowner rather than the insurance carrier. You should choose a company based on their reputation in the Glendale community and their expertise in handling local architectural styles.

Subrogation and Your Deductible

If your water damage was caused by a faulty product, like a brand-new dishwasher that leaked, your insurance company may pursue “subrogation” against the manufacturer. If they are successful in recovering the money they spent on your restoration, they are often required to refund your deductible to you. This process can take months or even years, but it is a nice financial bonus that can eventually offset your initial out-of-pocket costs.

Frequently Asked Questions (FAQs)

Will my insurance pay for a hotel while my Glendale home is drying?

Yes, most standard policies include “Additional Living Expenses” (ALE). This coverage pays for a hotel, restaurant meals, and other costs if a professional restoration company deems your home uninhabitable due to noise from equipment, high humidity, or the presence of contaminants.

Can I perform the cleanup myself and still get paid by insurance?

While you can technically do the work yourself, insurance companies often pay homeowners a much lower “self-pay” labor rate than they pay professional companies. More importantly, without professional equipment and documentation, you may fail to dry the home completely, leading to mold that insurance will likely refuse to cover later because you didn’t hire an expert initially.

What happens if mold is found during the water restoration?

Many policies have a “mold cap,” often limited to $5,000 or $10,000. If mold is discovered, your restoration contractor will need to file a separate “supplement” to the claim. It is always easier to get mold coverage approved if it is clearly a result of a sudden water event rather than a long-term leak.

Does insurance cover the cost of the plumber who fixed the pipe?

Interestingly, most policies cover the “resultant damage” (the flooded floors and walls) but do not cover the cost of the plumbing repair itself. You will likely have to pay the plumber out of pocket to fix the pipe, but the insurance will cover the thousands of dollars in drying and reconstruction costs.

What if the insurance estimate is lower than the restoration contractor’s?

This is a common occurrence. Your contractor will submit a “supplement” to the insurance company with photos and moisture data explaining why the extra work is necessary. In almost all cases, the adjuster and the contractor can reach an agreement based on the industry-standard pricing in Xactimate.

Trusting 4 Square Restoration with Your Glendale Insurance Claim

Navigating a water disaster is difficult enough without the added stress of an insurance dispute. By understanding how the claims process works and the importance of professional documentation, you can turn a catastrophic event into a manageable recovery. The key is to partner with a team that doesn’t just understand pipes and pumps, but also understands the language of insurance adjusters and the specific needs of the Glendale community. Protecting your home’s value and your family’s health requires a commitment to excellence that only a professional restoration firm can provide.

At 4 Square Restoration, we are more than just a cleanup crew; we are your advocates throughout the entire water damage restoration glendale ca process. Our team is expert in the documentation required by major carriers, and we work tirelessly to ensure that your claim is handled fairly and accurately. We utilize the latest 2026 drying technology and provide the meticulous reporting that adjusters need to approve your coverage. Whether you are dealing with a burst pipe in the middle of the night or a complex flood event, 4 Square Restoration is here to handle the technical details and the insurance paperwork so you can focus on getting your life back to normal. If you are facing a water damage crisis and need a partner you can trust with your insurance claim, contact 4 Square Restoration today to receive the professional care and expert advocacy your Glendale property deserves.